Effective inventory management for small businesses is about far more than just counting boxes on a shelf. It’s the day-to-day process of ordering, storing, and selling your stock in a way that directly fuels your profitability and keeps customers happy. Think of it as the command centre for all your physical goods, making sure your money is tied up in products that actually sell, not just gathering dust.

Why Smart Stock Control Is Your Secret Weapon

Picture your storeroom. Is it a chaotic pile of boxes or the well-oiled powerhouse of your business? That's the difference smart inventory management makes. For any small business in the UK, getting a firm grip on your stock is fundamental to survival and growth. It’s how you turn products on a shelf into healthy cash flow and happy, loyal customers.

It all comes down to making your money work smarter, not harder. Without a clear system, you're essentially just guessing how much cash to sink into products. This is a classic tripwire for new businesses, who either overspend on stock that won’t shift or, just as damagingly, run out of their most popular items and lose sales.

The Local Baker's Balancing Act

Let's take a local baker as an example. Their most vital ingredient is flour. If they order too much, it eats up precious space, locks up cash that could be spent on marketing or a new oven, and risks spoiling before it can be used. Every single bag of wasted flour is profit straight down the drain. This is overstocking, and its hidden costs can quietly cripple a small business.

On the flip side, what happens if the baker underestimates demand and runs out of flour on a busy Saturday morning? They can’t bake their best-selling sourdough loaves. Customers walk away empty-handed and annoyed, maybe even heading to the competitor down the road. That’s a stockout—a direct hit to your sales and your hard-earned customer trust.

Smart inventory management is the art of balancing these two extremes. It’s the practice of having just enough stock to meet demand without incurring the costs and risks of holding too much.

Nailing this delicate balance is what builds a more resilient and successful business. When you get it right, you ensure your capital is always working for you, not against you. For a deeper dive into the core concepts, this comprehensive guide to inventory management is a great place to start.

Navigating Today's Economic Climate

The need for razor-sharp stock control has become even more urgent for UK businesses. The period between 2018 and 2021 was marked by huge disruptions from Brexit, the pandemic, and serious supply chain meltdowns. For example, businesses typically stock up in the third quarter for the Christmas rush. Yet in 2021, retail stock levels grew by a mere £380 million—a figure far below normal, showing how supply chain problems directly capped business potential. You can find more detail on these economic impacts from the Office for National Statistics.

At its heart, solid inventory management delivers three core benefits that lay the groundwork for a thriving small business:

- Boosted Cash Flow: By steering clear of overstock, you free up cash that can be put to better use, whether that’s a new marketing campaign or training for your staff.

- Enhanced Customer Satisfaction: Keeping your best-sellers reliably in stock prevents lost sales and builds a reputation for dependability, which is key for bringing customers back.

- Increased Profitability: Cutting down on waste from expired or obsolete products and preventing sales losses from stockouts directly protects your bottom line.

Essential Techniques for Managing Your Stock

To truly get a handle on your inventory, you need to move beyond guesswork and start using a proven system. For a small business, adopting established techniques can feel like a big leap, but they're much simpler than they sound. Think of them as a clear framework for making smart decisions about your stock, helping you protect your cash flow and focus on what really matters.

Let's break down some of the most effective methods out there. We'll use real-world examples to show you exactly how you can put them to work for your own business.

Prioritise Your Stock with ABC Analysis

Let's be honest, not all of your stock is created equal. That's where ABC analysis comes in. It’s a straightforward way to categorise your inventory into three tiers based on how much value it brings to your business. This helps you put your time and money where they’ll make the biggest difference.

Imagine you run a small online boutique. Here’s how you might organise your stock:

- A-Items: These are your superstars—the high-value products that fly off the shelves. Think of those designer dresses that bring in the most revenue. They might only make up a small part of your physical stock (~20%), but they generate a massive chunk of your profit (~80%). These items demand constant attention and tight control.

- B-Items: This is your solid, mid-range inventory. These items are important but not critical, like your popular handbags and shoes. They're more numerous than your A-items but have a lower overall value. You'll want to review them regularly, just not with the same intensity as your top-tier products.

- C-Items: These are your low-value, high-volume products. Think accessories like scarves or basic socks. They take up the most space but contribute the least to your bottom line. You can get away with counting these less frequently, freeing up valuable time.

Using ABC analysis is all about working smarter, not harder. It ensures your most profitable products are always looked after and never out of stock.

Use FIFO to Keep Products Fresh

First-In, First-Out (FIFO) is a non-negotiable technique for any business selling perishable or time-sensitive goods. The idea is simple: the first items you get into your inventory should be the first ones you sell. This system makes sure older stock gets moved out before it expires, spoils, or just goes out of style.

A local coffee shop is a perfect example. The bags of coffee beans that show up on Monday absolutely must be sold before the new delivery arrives on Friday. By organising their shelves so the oldest stock is always at the front, they cut down on waste and make sure every customer gets a fresh, top-quality product.

But it’s not just for food. This method is a lifesaver for businesses that sell electronics, cosmetics, or anything with a warranty or a short fashion cycle. If you find yourself with extra stock that needs careful organisation, off-site storage can be a huge help. For anyone considering this route, here are some essential tips for choosing a self storage unit to keep your inventory safe and organised.

Reduce Waste with Just-In-Time (JIT) Ordering

The Just-In-Time (JIT) method is all about ordering stock from suppliers only when you actually need it—either for production or to fill a customer's order. The whole point is to keep the amount of inventory you're holding to an absolute minimum, which drastically slashes storage costs and the risk of being left with unsellable dead stock.

JIT flips your inventory management from a "just in case" mindset to a "just in time" one, aligning your stock levels perfectly with what your customers are actually buying.

This approach takes a lot of coordination. You need reliable suppliers and a pretty good idea of what your demand will be. A custom furniture maker, for example, might only order specific wood and fabric after a customer has placed and paid for a bespoke chair. This completely avoids the cost of storing materials that might never get used.

For businesses that are always on the move, managing stock in transit presents its own unique set of problems. Thankfully, there are great solutions to help you optimise mobile inventory with van racking and keep your products secure and organised on the road.

Common Inventory Pitfalls and How to Sidestep Them

Even the most organised small businesses can get tripped up by simple inventory mistakes. These seemingly minor slip-ups often snowball, costing you money, space, and—worst of all—your customers' trust. Successfully navigating the world of inventory management for small businesses means knowing what these common pitfalls look like and having a plan to steer clear of them.

So, let's pull back the curtain on the hidden dangers that can undermine all your hard work. We'll get real about the true cost of overstocking, the damage of constant stockouts, and how poor forecasting can quietly sabotage your growth. For every mistake, we'll give you a clear, actionable solution to help you build a more robust, error-proof system.

The Hidden Danger of Spreadsheets

For many new businesses, a spreadsheet feels like a sensible, low-cost place to start tracking stock. And while it’s certainly better than nothing, relying on manual data entry is like walking a tightrope without a safety net. Human error is practically guaranteed. A single misplaced decimal or a forgotten entry can throw your entire stock count into disarray, leading to incorrect orders and baffling financial figures.

As your business grows, these spreadsheets become slow and unwieldy. The biggest problem? They don't offer real-time updates. The information you're looking at could be hours or even days out of date, making it impossible to react quickly to a sudden sales spike or a low-stock warning.

Overstocking: The Cash Flow Killer

Having too much stock might feel like a safe bet, but it's one of the most expensive mistakes a small business can make. Overstocking ties up your cash in products that are just sitting on a shelf, money that could be invested in marketing, new equipment, or other growth opportunities. It also inflates your storage costs, as you need more physical space to hold everything.

If you find yourself struggling with space, exploring professional Exeter self storage options can be a flexible way to manage excess inventory without the commitment of a larger warehouse.

This is a surprisingly common issue in the UK. Even among the 15% of small and medium-sized businesses aiming for lean inventories to keep costs down, many still find themselves drowning in unsold goods. In fact, research shows that only 27% of businesses with over 20% excess stock manage to redistribute it effectively. Instead, a whopping 74% resort to promotional sales to clear it out—a strategy that can seriously erode your profit margins over time. You can learn more from Netstock's inventory management report.

Stockouts: The Customer Repellent

The flip side of the coin—running out of popular items—is just as damaging. A stockout isn't just a missed sale; it's a broken promise to your customer. When a shopper is ready to buy but finds the item unavailable, they don't just wait around. A huge 69% will go directly to a competitor.

Every stockout is a direct invitation for your customers to discover another brand. Consistently failing to meet demand erodes trust and makes it nearly impossible to build a loyal customer base.

This is where a little foresight goes a long way. Implementing safety stock levels for your best-sellers provides a crucial buffer against unexpected demand surges or supplier delays. It’s a simple move that helps you keep your promises and your customers.

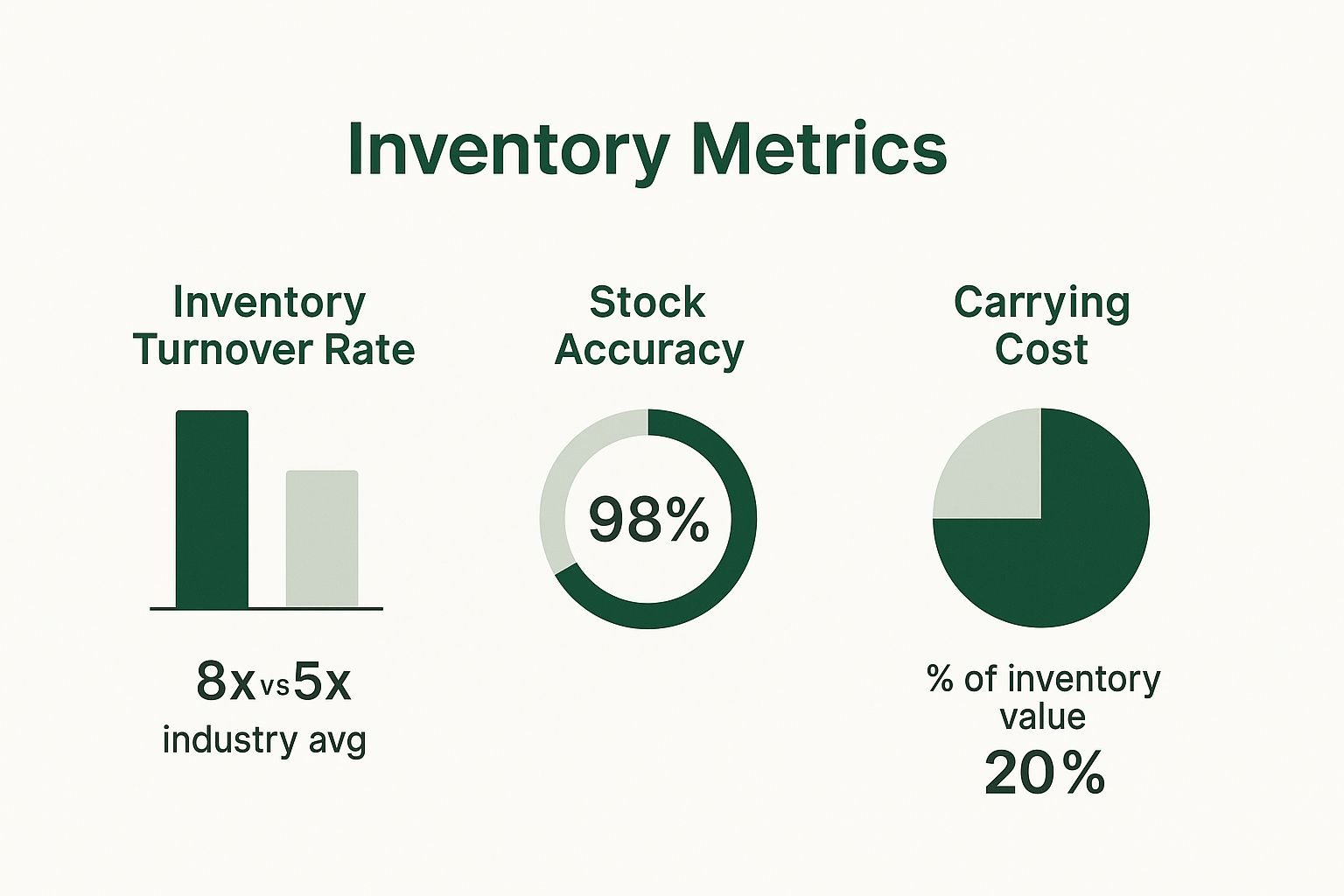

To help you visualise this, here’s a look at how top-performing businesses manage their stock compared to the average.

The data speaks for itself. The most efficient companies maintain high stock accuracy and turnover while keeping carrying costs low—a delicate balance that prevents both overstocking and stockouts.

It's easy to fall into these inventory traps, especially when you're juggling a dozen other tasks. But by understanding the risks, you can take simple steps to protect your business.

Let’s break down some of the most frequent mistakes we see small businesses make and how to get ahead of them.

Common Inventory Mistakes vs Proactive Solutions

| Common Mistake | Potential Consequence | Proactive Solution |

|---|---|---|

| Relying on Manual Spreadsheets | Inaccurate data from human error, slow to update, no real-time visibility. | Invest in Inventory Software: Adopt a system that automates tracking, provides real-time data, and integrates with your sales channels. |

| No Regular Stock Counts | Discrepancies between recorded and physical stock (shrinkage), leading to surprise stockouts. | Implement Cycle Counting: Schedule regular, partial stock takes instead of one big annual count to catch errors early. |

| Ignoring Sales Data | Poor purchasing decisions, leading to either overstocking unpopular items or running out of best-sellers. | Use Data for Forecasting: Analyse historical sales data to identify trends and predict future demand more accurately. |

| Keeping Too Much "Just-in-Case" Stock | Ties up cash flow, increases storage costs, and risks products becoming obsolete or expiring. | Set Reorder Points: Use sales velocity and lead times to calculate the ideal time to reorder, minimising excess stock. |

| Forgetting About Safety Stock | Unexpected demand spikes or supplier delays lead to stockouts and lost customers. | Calculate and Hold Safety Stock: Maintain a small buffer for your most popular products to cover unforeseen events. |

These proactive solutions aren't about adding more work to your plate. They're about working smarter. By shifting from reactive fixes to a more strategic approach, you can build a resilient inventory system that supports your business's growth instead of holding it back.

Choosing The Right Inventory Management Technology

Making the leap from a spreadsheet to dedicated software is a huge moment for any small business. It’s when you stop just reacting to stock levels and start proactively managing them. This section is all about helping you make that choice without the stress, ensuring you pick a tool that genuinely simplifies your operations.

We'll walk through the different kinds of technology out there, from simple barcode scanners to full-blown cloud-based systems that plug right into your sales platforms. Getting this right now will save you a world of headaches and money down the line, setting your business up for proper growth.

From Simple Scanners To Integrated Systems

The tech you need really comes down to the size and complexity of your business. For a tiny operation, a simple mobile app paired with a barcode scanner might be all it takes to get your stock counts digitised and slash manual errors. It's a low-cost starting point that’s immediately more accurate than pen and paper.

But as you grow, the real power is in cloud-based inventory management systems. Think of these platforms as the central brain for all your stock information. They can connect directly to your e-commerce site, point-of-sale (POS) system, and even your accounting software, giving you one single, truthful view of your inventory across every channel.

That integration is everything. It means when a customer buys something from your online shop, the stock level updates everywhere automatically. No more accidentally selling the same item twice.

Key Features To Look For

When you're sizing up different software, there are a few features that are non-negotiable for effective inventory management for small businesses. You need a solution that does more than just count things.

Your checklist should include:

- Real-Time Tracking: The system has to update stock levels instantly across all sales channels the moment a sale happens or new stock arrives.

- Low-Stock Alerts: Get automatic notifications when an item's quantity drops below a level you've set, so you can reorder before you're caught out.

- Sales Analytics and Reporting: Access to data on your bestsellers, slowest movers, and profit margins helps you make much smarter buying decisions.

- Multi-Location Support: If you operate from more than one place—like a shop and a small warehouse—the software must track stock for each location separately. If you're using off-site storage, our guide on https://mgselfstorageexeter.co.uk/blog/mg-self-storage-your-solution-for-spacious-storage-units-in-exeter/ can show you how this fits into a bigger strategy.

For businesses with more complicated product lines, looking into advanced tracking can be a game-changer. For instance, using RFID tags for inventory control offers massive benefits, especially for UK retailers dealing with high-volume or high-value goods like clothing.

A Practical Checklist Before You Invest

Committing to new software is a big investment, so it pays to ask yourself a few direct questions first. Your answers will help you find a system that fits what your business genuinely needs, not what a salesperson says you need.

Despite its importance, adopting modern inventory management software remains surprisingly low. Recent statistics indicate that only around 22% of small businesses in the UK have invested, often due to cost concerns. This reliance on manual tracking contributes to inventory distortions that cost businesses globally an estimated £1.3 trillion annually, with 35% of businesses losing sales by mistakenly selling out-of-stock products. For more details on these findings, you can discover more insights about inventory management statistics.

Use this checklist to make sure you’re making a smart decision:

- What is my budget? Prices can range from about £30 per month for basic plans to several hundred for more advanced systems. Be realistic about what you can afford, but also think about the long-term cost of not having an efficient system.

- How complex is my inventory? Are you selling a handful of products or thousands of variations (SKUs) with different sizes and colours? The more complex your stock, the more powerful your software needs to be.

- Does it integrate with my existing tools? Check that the software connects smoothly with your e-commerce platform (like Shopify or WooCommerce), your POS system, and your accounting software (like Xero or QuickBooks).

- Will it support my future growth? Choose a solution that can grow with you. A system that seems perfect today might feel tight and restrictive in two years if you plan on adding more products or opening new sales channels.

Choosing the right technology is a fundamental step in building a resilient and profitable business. It empowers you to move from guessing to knowing, turning your inventory from a potential headache into your greatest asset.

Your Step-by-Step System Implementation Plan

You’ve picked out your tools and decided on the best techniques. Now comes the exciting part: putting it all into practice. A smooth switch to a new inventory system hinges on a clear, methodical plan. It's the only way to avoid operational chaos and start seeing the benefits from day one.

This practical guide will help you minimise disruption and set your business up for long-term success. Follow these steps, and you’ll build a solid foundation for your new and improved stock control process.

Step 1: Conduct a Full Physical Stocktake

Before you can move forward, you need a crystal-clear picture of where you are right now. The first, and most critical, step is to conduct a complete physical stocktake of every single item you hold. Think of this as your "ground zero"—an accurate baseline count that you'll feed into your shiny new system.

An inaccurate starting point will sabotage your entire setup, creating phantom stock and discrepancies from the get-go. Choose a time to minimise disruptions, like closing for a day or doing the count after hours. Most importantly, make sure you have enough hands on deck to get it done efficiently and accurately.

Step 2: Organise Your Storeroom

A well-organised storeroom is the physical backbone of any good inventory system. Before you dive into the software, take the time to clean, sort, and logically arrange your stock. This is the perfect chance to make your inventory easy to find, count, and manage.

Consider these simple organisational tips:

- Group Similar Items Together: Keep all variations of a single product in one place. This makes picking and counting a breeze.

- Implement Clear Labelling: Use consistent, easy-to-read labels for shelves, bins, and aisles. This helps your team find items and put new stock away correctly every time.

- Apply the FIFO Principle: If you deal with perishable or time-sensitive goods, set up your shelving so the oldest stock is at the front and gets picked first.

A logical layout directly cuts down the time it takes to fulfil orders and do stock checks. For businesses finding they're running out of room, using flexible business storage can be a brilliant way to keep inventory organised without the commitment and cost of a larger commercial lease.

Step 3: Set Up Your Software and Input Data

With an accurate stock count and an organised storeroom, you're ready to get your chosen software up and running. This phase involves customising the system to fit your business like a glove, from setting up product categories and locations to inputting supplier details.

The most time-consuming but essential part of this step is entering your product data. This usually involves creating a unique SKU (Stock Keeping Unit) for each product variation.

A SKU is a unique code that identifies each distinct product and its variants, like size and colour. Consistent SKUs are the language your inventory system speaks to track everything with precision.

Next, enter the baseline counts from your physical stocktake. Double-check everything. Then check it again. Even tiny data entry errors at this stage can snowball into major headaches down the line.

Step 4: Train Your Team Thoroughly

A new system is only as good as the people using it. Proper team training isn’t just a good idea—it’s non-negotiable for a successful rollout. Every team member who handles stock, from the person receiving deliveries to the one packing orders, must understand the new processes inside and out.

Your training should cover:

- How to correctly receive and log new stock.

- How to find items and update quantities after a sale.

- The importance of following the system consistently, without cutting corners.

Make sure your team understands why these changes are happening. When they see the benefits for themselves—like fewer stockouts and less time wasted searching for items—they'll be much more likely to get on board. This buy-in is absolutely vital for maintaining data accuracy and keeping things running smoothly for the long haul.

Frequently Asked Questions About Inventory Management

As a small business owner in the UK, figuring out the world of stock control can bring up a lot of questions. Getting clear answers is key to setting up a system that actually works. Here are some of the most common queries we see, answered to help you master inventory management for small businesses.

How Often Should I Do a Physical Stock Count?

For most small businesses, a full physical stock count at least once a year is a must for financial reporting. But for much better day-to-day accuracy, many businesses use cycle counting. This just means counting small, manageable sections of your inventory on a daily or weekly rota.

This approach is far less disruptive than shutting everything down for an annual count. Better yet, it helps you spot discrepancies almost as soon as they happen. The result? More accurate stock records all year round, which means fewer surprise stockouts and happier customers.

What Is the Difference Between Inventory and Warehouse Management?

It helps to think of it this way: inventory management is the "what," and warehouse management is the "where."

- Inventory Management: This is all about the numbers and decisions. It covers tracking stock levels, forecasting what customers will want, and deciding when to reorder products. It's the financial and analytical brain of your operation.

- Warehouse Management: This is the hands-on, physical side of things. It's about how you store, organise, pick, pack, and ship those products from your shelves.

When you're a tiny business, these two roles often feel like the same job. But as you grow, understanding the difference is crucial for keeping things running smoothly and efficiently.

Inventory management is the strategic thinking behind your stock, while warehouse management is the physical execution of those plans in your space.

Is It Okay to Just Use a Spreadsheet?

You can absolutely start with a spreadsheet. If you only have a handful of products, it can be a perfectly fine way to get going. But be warned: spreadsheets are famous for human error, they don't update in real-time, and they're missing essential features like low-stock alerts or sales analytics.

As your business grows, the time you'll sink into manually updating a spreadsheet – and the cost of the inevitable mistakes – will quickly add up. Soon enough, it will far outweigh the price of an entry-level inventory management software.

What Is a Good Stock Turn Rate for a Small Business?

Honestly, there’s no single "good" number. It varies massively from one industry to another. A local greengrocer will have an incredibly high turnover, while a bespoke furniture shop will naturally have a much lower one. The trick is to benchmark your rate against your industry's average and then focus on improving it over time.

A rising stock turn rate is generally a great sign. It means you're selling products well and managing your stock efficiently, without tying up too much precious cash in goods that are just sitting on a shelf.

Managing stock effectively often comes down to having the right amount of space. If you're struggling with overstock or need a secure place for your inventory as your business grows, MG Self Storage can help. We offer flexible, secure, and accessible business storage solutions tailored to your needs. Visit us at https://mgselfstorageexeter.co.uk to see how we can support your business.